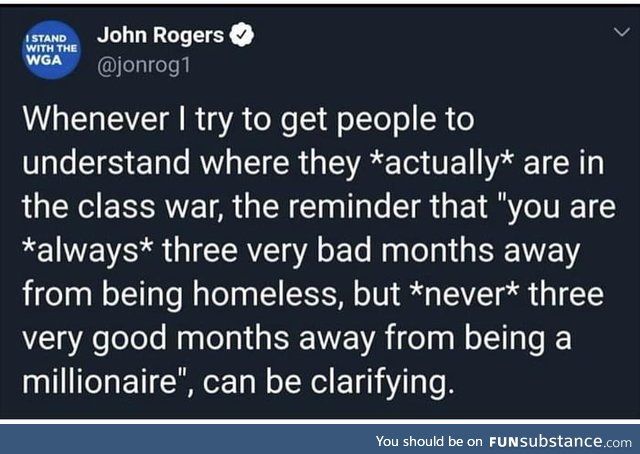

I mean- yes. Strictly speaking- you could win the lottery-

Improbable but possible- and be a multi million or even billion aire in 3 months. So the guy’s statements aren’t correct. Likewise- it’s a foolish proposition that has nothing to do with class wars- it’s reality. It’s easier to destroy than create. One can spend money faster than one can make it. You can burn homes faster than they can be built- it takes seconds to kill a person but 9 months to grow a baby and 18 more years minimum to make an adult. None of that is about the class war- it’s just how the world works.

Reducing everything to class is intellectually lazy, but a useful shorthand for where you are in our society. I believe the more useful lesson is to remember that you are not wealthy, and the money and assets you do have will not save you against catastrophe like it would a millionaire.

The moment you realize millionaires aren't a part of the class struggle, and have never been (at best they get replaced), and you're actually doing is having people who 3 months from being homeless attacking those who have 4 month safety margin.

People can’t conceptualize how little a million dollars is. To a person living on $50,000 a year- a million dollars in the bank is 20 years (gross) wages. If they don’t change their spending habits by much that is. In that sense- sure it is a lot. But.... it isn’t really. If you stuff it in a savings and use it to keep the same lifestyle but not work- it isn’t transformative alone. Your life is the same but you have more time. Time to be bored- time to spend more money staying not bored, time to spend more on electricity at home or gas at home, fuel for your car, or whatever else you fill your time with where you used to be at work for these big chunks of the day. You could volunteer, or get a job doing work you enjoy or find fulfilling-

you’d have some freedom to not have to take jobs based on salary alone etc- but you’d also only have 20 years- to a teen, 20,30 year old- when the money runs out you have a whole life left. For a 50+ year old- you’ll be into retirement when that money runs out. Either way- you’d need to work to make sure you would have money when it went dry.

You could invest- but a million dollars actually isn’t that much to invest unless you pick something pretty high risk. Starting a business for example- very high risk. You won’t likely be able to take that million and place it into stable stocks or other avenues that will near guarantee you’d get a $50k return a year. You’re still likely going to work, you’re still likely needing to advance your skills and network and education and advance your career just as if you didn’t have the money- with the exception being that you may have some safety net and accumulate a nice little nest egg. With a couple major caveats...

1. It’s called “liquidity.” If you put your million in a bank or a mattress or whatever- in cash- it will for all intents not go up or down unless you take money out. If you need it ever- it is right there. But... if you invest your million- on paper you’re worth a million- maybe more. But.... you do t have access to it. In an emergency you can’t just take what you need. You’ll have to sell assets, convert them to cash. In a hurry that can mean losses and it can be tax liability. It will also likely hurt your long term financial plans- and could even completely end your nest egg just the same as someone without the million- you get one “free pass” to disaster they don’t have- after that you’re the same as them mostly.

Adding to that- if you don’t invest your million- keep it in a bank or pillow case whatever- there will always be that million there f you never touch it- but in 10,20,30 years your million will not be worth what it was. Inflation. Simple. In 30 years a gallon of gas went from about 25 cents to almost $4. Bread went up 300%. A QPC with cheese meal at McDonald’s was $5 20 years ago and is about $10 now. So your million goes down in value over time even if it is still a million. If you want it to have the same buying power in decades you have to grow it.

What’s more- if you choose an option that indexes you to draw the $50k off the mill for 20 years- you don’t increase your “salary” as you age- so not only would someone else who stayed in the workforce conceivably be making twice as much as you in 20 years- your $50k salary isn’t worth as much. In 1980 $40k salary was VERY comfortable most places- the average was closer to $25k. In 2010 $40k was at or below the poverty line in many places, and in most others barely middle class.

2. You have to not change your spending habits. That’s REALLY hard. Especially when you have a million on the bank. The housing meltdown in America showed a huge number of American families were overstretched. You aren’t going to be able to save a nest egg or emergency fund if you’re paying 50%+ of your salary for your home. And it isn’t that they were “duped” so much- it’s that many people just didn’t want to go with less. People love beyond their means. It sounds harsh and I don’t mean it so- but if that 2 bedroom or 1 bedroom or whatever- is 50% of your salary- share rooms. Get a studio. Rent. Live in a trailer. It sucks. It’s inconvenient and unpleasant.

Ask the many immigrants and others living 6 people to a 1 or 2 bedroom if it’s fun. It isn’t. But as much as it’s nice for the kids to have their own room or for no one let alone a whole family to share a living room- they can’t afford it, and if you’re spending 50% of your income on housing- neither can you. I understand. If you’re in some markets- a studio can cost 50% or more of a minimum wage workers income. It socks sharing a studio with room mates- but man.... people do what they have to to get where they want to be or just survive.

In many markets a million won’t even buy you a home. It’s really not a lot of money- you could give the entire population of a small town $100 each. That’s less than a penny for each American. And when you have money- you want to spend it. Say you keep your job- you’re making $50k and have $50k a year to draw on or $X in investment income on top- so let’s say you’ve gone from $50 to $100k a year. You’re not going to spend any of it?

You aren’t going to get a nicer place, pay off your loans, buy a better car, get that new phone, fix your rotting deck or leaky pipes? What happens to your tax return every year? Where does that money go if you get one? What have you already invested in? How much is in your 401k?

These are habits, budget, discipline, goals. These aren’t things having money suddenly gives you. These are things that people who earn money tend to have (or have someone who does it for them...) and they’re needed to KEEP money. But most people can’t do it. It’s a documented phenomenon. We get used to money. Our lifestyles tend to increase with earnings. It’s harder to say no to ourselves when we can actually say yes if we wanted to be. Harder still when we have more money than we can conceive running out.

Give a small kid $100- a kid used to maybe $10 on birthdays- they’ll think that money will buy everything they ever wanted at the toy store. $5 for candy here, $10 for a new action figure there, $20 for a nerf gun or an art set... and before they know it they only have a few dollars left. The popular “make your own coffee” life hack shows us this. A pack a day smoker is spending $300 a month on name brand cigarettes in a place like New York. If you have a Starbucks a day that is closer to $100 a month.

Overall having a million in the bank is nicer than not- but it also as you say- is far from being “safe”- especially if your lifestyle matches your income. If you make solid 6 figures a year, have a million plus dollar home and 5 kids, 3 in college, 1 graduated, and one on the way to college- you’ve got a $30 or $40 k car each for you and the spouse (nothing too fancy- those are mid to low end pricing for most sedans and such now days..) it wouldn’t take much to find yourself in dire straights. You’ve got thousands in student loan debt a month, you’ve got thousands in car payments and mortgage, that’s without any credit card debt or other factors. That’s without one or more of your kids getting in trouble or needing help. That is without school trips and phone bills and insurance and so on and on.

It sounds inconceivable that people with “so much money” could have financial hardship or worries. Most people would feel it is laughable to feel for them or include them as with the “common man,” but just because they seem to have more doesn’t mean they really have so much more. Nowadays a million isn’t really much. Most people probably know at least one millionaire.

Class war?

You've probably no idea how good you have it by almost any standard you choose

Improbable but possible- and be a multi million or even billion aire in 3 months. So the guy’s statements aren’t correct. Likewise- it’s a foolish proposition that has nothing to do with class wars- it’s reality. It’s easier to destroy than create. One can spend money faster than one can make it. You can burn homes faster than they can be built- it takes seconds to kill a person but 9 months to grow a baby and 18 more years minimum to make an adult. None of that is about the class war- it’s just how the world works.