1. Don’t condemn somebodies beliefs because you don’t have them

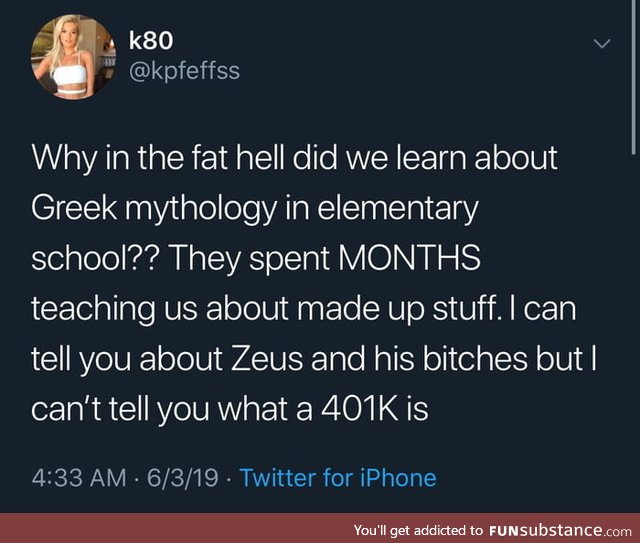

2. What is a 401K, I hear it all the time but it’s like they’re saying wing-wam-banana-flam

401(k) is the section of law that set up individual retirement accounts. 401k’s are governed by law because the government gives you tax breaks if you use one.

401Ks are pre-tax, meaning whatever you give to your 401k is not counted as income when the government takes their cut of your check.

Companies also usually match what you give, so they basically give you extra money (be very clear about the timeline of this “gift”, since they usually take it back if you don’t stay for enough years).

Unlike FICA contributions, this money actually belongs to you, and you can move it when you change jobs. You can also have your own 401K.

Because it’s supposed to be for retirement, there are penalties if you take it out early except in specific instances.

Just as an FYI, each of these sentences break down into more. They also are arguable, especially down tangents related to what the government and/or you “should” do. But that’s enough to get going.

Your HR department will be happy to explain about 401k, as this likely will increase your engagement/tenure; or they will refer you to the 401k folks who will break it down for you. It’s possible to scam people on 401k’s, probably, but not at that level (except the fees for managing, which is not a scam but should be understood upfront) so their only skin in the game is helping you.

One thing I didn’t say is that 401k’s are investing, almost always in the Stock Market. You can have low, mid-level or high fees for 401Ks, based usually on how much the mix of stocks, bonds, etc are managed for you. You can also have lower, moderate, or high risk. Sometimes the options are very simple, like you just pick a risk profile or they decide for you based on your age (example: high risk is not recommended for people retiring in 5 years). Sometimes they are more complex and it can feel a bit overwhelming. Be brave, ask for help, and let time build you a nice little pot of money.

Yes. In less technical terms a 401k USA type of investment plan for your retirement or need. You put money from your earning into it like a savings account, but you aren’t charged pay or income tax on the money. Its used to buys stocks or bonds, and the money that makes is put back into the “savings account.” When you reach retirement age you can take the money you’ve earned out and live on it- and you have to pay the taxes on the money when you take it out. You can also borrow money from it for certain qualified reasons- money you pay yourself back for. The interest rate is much better than a savings account but there is some risk because it’s stocks and bonds so if the market does poor you can loose money- it’s just relatively very low risk.

Unlike trading stocks normally you don’t deal with gains taxes etc. and because you get to take the money out before payroll tax you can lower what you owe in taxes every year. You do pay tax when you take the money out, but with planning and luck you can take it out when the tax rate is lower so instead of paying a higher tax now you can pay a lower tax later. Many employers offer plans which make it very simple. You just sign some forms and tell them how much to take from each check. Most 401k plans are offered through investment firms and if your employer doesn’t offer a plan you may be able to contact a firm directly. There are also other types of plans like Roth IRA etc. it sounds complex but isn’t. There’s usually a management fee for the plan but that’s deducted from the amount in the plan and you generally don’t actually pay any money out of pocket for it.

There's also usually company options when it comes to the stocks, so if you have faith in your company, just going with the stock options makes sense. They'll also only match contributions up to a point though, so if you have enough where you can hit the match cap and then diversify the rest of your portfolio, you're doing yourself two favors.

Teachers are focused on providing info they feel good at. It’s not so easy to be an expert at 401Ks. I mean, would YOU rather teach fun, easy-to-present dramatic stories or learn and teach real world stuff?

Also - no one will argue with you about a dead religion; why we settled on Greek instead of Norse or African is a whole other thing.

People will argue with you PLENTY about statements as seemingly non-controversial as “saving is good” and “staying in budget” or “find a job that can pay the bills for the area you want to live in”.

It’s a repeat of the national retirement income system, basically, but private and individually driven. There’s a strain of Americanism that believes the government won’t do a good job, so we repeat systems as public and private.

Well- sort of. Americans have public benefits for retirement, but what they pay isn’t going to have you retired and living in a huge house and owning a fleet of toys and traveling to far away lands. So a 401k is a way that you can put money away as a private citizen that doesn’t count against you now like savings will- and let’s you plan to meet what expenses you think you’ll have in excess of public benefits. Basically it can act as an extra security but it’s also a way to make sure you can have the lifestyle you want when you retire.

What you are learning is ancient history and part of another culture. To be a well rounded adult you need to understand how and why things happen and not just a bunch of details without context. Greek mythology shaped the ancient world which shaped the modern world and we can still see the influences of those ripples in modern society. The world is a complex web and not just a bunch of disconnected pieces. You can know everything about the engines of an airplane but if you don’t know about the electrical systems and computer systems and controls- you can’t design or repair an aircraft. The world is like that. One thing here, is linked to some seemingly random thing there.

Schools, especially American schools, often don’t teach enough about the rest of the world. A world we live in and are a part of an increasing global community. How many people educated in America even understand the political systems, geography, culture, or history of our border neighbors we share a continent with- Mexico and Canada? I can teach you in a day how to follow a checklist to repair a bad circuit and now you’re a robot. A useless monkey that can do one thing and can follow basic instructions. Teaching you about electricity and electronics will take much longer, and it won’t give you step by step instructions to fix your exact problem- but I’ve given you all the tools to figure out yourself how to fix any problem you encounter with electrical and to build so you can do more advanced things.

Simply typing a question about a 401k into google takes as much time as posting a complaint about not knowing and will teach you all the basics and where to get more info if you want- but in under 5 minutes you’ll have everything you need to know to get started. It’s simple and an idiot can pay someone to do it for them. There’s no need to waste time on that. An education in our system isn’t meant to produce a human being with an instruction book for life. It’s meant to give you the tools to find your own way. Any moron can follow instructions.

Almost Everyone thinks they are smart and capable and “special.” You have the tools. Use them. What shows your true ability is what you can do without having someone draw it in crayon for you. Figuring things out for yourself is a crucial skill. Figure it out. No one is going to hand you a book that contains everything tailored made to solve every problem you’ll ever encounter in life and be rich and happy. You build your life and your intelligence, ability, and drive partially dictate the results.

Is that why you won't check my math?!

Anyway, I'm pretty sure I figured out my flaw. I cubed it when I should have just squared it and then taken into account altitude as the 3rd variable as that's not arcseconds, and then use some trig, specifically parallax to figure the rest out. At least I knew I was off lol. I'll work on it later, once I'm drunk again, just for fun... but that stuff is like 100 comments ago in that Super-Villain chat... so... whatever, at least I knew I was off and had the balls to ask for help XD

I'm only now learning about Greek gods from studying Ancient Greece ... Why would that stuff be taught so early on since so much of it is cheating and stuff?

They told us cuz they will be back in the days of dry bones. These days last think anyone wants is a 41K.

Not sure the school you went to but in my home state we all knew, why you didn't take a business class says a lot about you!

Only Economics (intro to macro and micro) was offered at my HS, and there were only 30 spots. I ace'd it while playing pokemon and going out of my way to let people cheat off me (I found this hilarious, given the subject matter).

Had they offered Calculus II, Statistics II, Accounting or Business law in HS, I would have taken all of them.

Comments

2. What is a 401K, I hear it all the time but it’s like they’re saying wing-wam-banana-flam

401Ks are pre-tax, meaning whatever you give to your 401k is not counted as income when the government takes their cut of your check.

Companies also usually match what you give, so they basically give you extra money (be very clear about the timeline of this “gift”, since they usually take it back if you don’t stay for enough years).

Unlike FICA contributions, this money actually belongs to you, and you can move it when you change jobs. You can also have your own 401K.

Because it’s supposed to be for retirement, there are penalties if you take it out early except in specific instances.

Just as an FYI, each of these sentences break down into more. They also are arguable, especially down tangents related to what the government and/or you “should” do. But that’s enough to get going.

One thing I didn’t say is that 401k’s are investing, almost always in the Stock Market. You can have low, mid-level or high fees for 401Ks, based usually on how much the mix of stocks, bonds, etc are managed for you. You can also have lower, moderate, or high risk. Sometimes the options are very simple, like you just pick a risk profile or they decide for you based on your age (example: high risk is not recommended for people retiring in 5 years). Sometimes they are more complex and it can feel a bit overwhelming. Be brave, ask for help, and let time build you a nice little pot of money.

Also - no one will argue with you about a dead religion; why we settled on Greek instead of Norse or African is a whole other thing.

People will argue with you PLENTY about statements as seemingly non-controversial as “saving is good” and “staying in budget” or “find a job that can pay the bills for the area you want to live in”.

Anyway, I'm pretty sure I figured out my flaw. I cubed it when I should have just squared it and then taken into account altitude as the 3rd variable as that's not arcseconds, and then use some trig, specifically parallax to figure the rest out. At least I knew I was off lol. I'll work on it later, once I'm drunk again, just for fun... but that stuff is like 100 comments ago in that Super-Villain chat... so... whatever, at least I knew I was off and had the balls to ask for help XD

Not sure the school you went to but in my home state we all knew, why you didn't take a business class says a lot about you!

Had they offered Calculus II, Statistics II, Accounting or Business law in HS, I would have taken all of them.